Tuesday, August 31, 2010

NEW YORK'S TALLEST BUILDING< ONCE AGAIN

Tower would rival Empire State Building

Look at Manhattan from afar, and the first thing you notice is the Empire State Building, spiking like a needle above the carpet of skyscrapers that coats Manhattan from tip to tip.

Now it has some competition — a proposal for a nearby glass office tower that would rise almost as high and alter the iconic skyline.

Now it has some competition — a proposal for a nearby glass office tower that would rise almost as high and alter the iconic skyline.

The tower would spoil the famous view of the 102-story skyscraper for millions of tourists, the Empire State Building’s owner, Anthony Malkin, testified yesterday at a City Council hearing. It “defines New York,’’ he said.

“We view this as an assault on New York City and its iconography,’’ said Malkin. It’s “the end of the image of New York City that billions of people hold dear.’’

The City Council is to vote this week on whether to allow a developer to erect a 67-story tower that is 34 feet lower than the 79-year-old Empire State Building, the city’s tallest skyscraper.

The proposed tower’s developer, David Greenbaum, says 15 Penn Plaza would provide critically needed and state-of-the-art office space to midtown Manhattan, creating at least 7,000 new jobs.

“The fact is, New York City’s skyline has never stopped changing, and I certainly hope it never will,’’ testified Greenbaum, president of Vornado Realty Trust’s New York chapter.

The council’s Zoning and Franchises subcommittee planned to vote today on whether to change rules. If they OK the plan, the final word would lie with the City Council — unless Mayor Michael Bloomberg, who holds veto power, objects.

The building would stand two blocks west of the Empire State Building on the site of the current Hotel Pennsylvania on Seventh Avenue, steps from Madison Square Garden and Penn Station.

“Wow! Wouldn’t that be sad!’’ said Christa Huggins, a 35-year-old from Utah visiting the Empire State Building’s observatory on the 102d floor.

Huggins said she “loves the view of New York all the way around, but especially in that direction. And this would block it.’’

Look at Manhattan from afar, and the first thing you notice is the Empire State Building, spiking like a needle above the carpet of skyscrapers that coats Manhattan from tip to tip.

The tower would spoil the famous view of the 102-story skyscraper for millions of tourists, the Empire State Building’s owner, Anthony Malkin, testified yesterday at a City Council hearing. It “defines New York,’’ he said.

“We view this as an assault on New York City and its iconography,’’ said Malkin. It’s “the end of the image of New York City that billions of people hold dear.’’

The City Council is to vote this week on whether to allow a developer to erect a 67-story tower that is 34 feet lower than the 79-year-old Empire State Building, the city’s tallest skyscraper.

The proposed tower’s developer, David Greenbaum, says 15 Penn Plaza would provide critically needed and state-of-the-art office space to midtown Manhattan, creating at least 7,000 new jobs.

“The fact is, New York City’s skyline has never stopped changing, and I certainly hope it never will,’’ testified Greenbaum, president of Vornado Realty Trust’s New York chapter.

The council’s Zoning and Franchises subcommittee planned to vote today on whether to change rules. If they OK the plan, the final word would lie with the City Council — unless Mayor Michael Bloomberg, who holds veto power, objects.

The building would stand two blocks west of the Empire State Building on the site of the current Hotel Pennsylvania on Seventh Avenue, steps from Madison Square Garden and Penn Station.

“Wow! Wouldn’t that be sad!’’ said Christa Huggins, a 35-year-old from Utah visiting the Empire State Building’s observatory on the 102d floor.

Huggins said she “loves the view of New York all the way around, but especially in that direction. And this would block it.’’

Monday, August 30, 2010

REAL ESTATE TRENDS: A change in home values

Analysts say era of wild rises is over.

Housing will eventually recover from its great swoon. But many real estate experts now believe that home ownership will never again yield rewards like those enjoyed in the second half of the 20th century, when houses not only provided shelter but also a plump nest egg.

The wealth generated by housing in those decades did more than assure the owners a comfortable retirement. It powered the economy, paying for the education of children and grandchildren, keeping the cruise ships and golf courses full and the restaurants humming.

More than likely, that era is gone for good.

“There is no iron law that real estate must appreciate,’’ said Stan Humphries, chief economist for the real estate site Zillow. “All those theories advanced during the boom about why housing is special — that more people are choosing to spend more on housing, that more people are moving to the coasts, that we were running out of usable land — didn’t hold up.’’

Instead, Humphries and other economists say, housing values will only keep up with inflation. A home will return the money an owner puts in each month, but will not multiply the investment.

Dean Baker, codirector of the Center for Economic and Policy Research, estimates that it will take 20 years to recoup the $6 trillion of housing wealth that has been lost since 2005. After adjusting for inflation, values will never catch up.

Housing will eventually recover from its great swoon. But many real estate experts now believe that home ownership will never again yield rewards like those enjoyed in the second half of the 20th century, when houses not only provided shelter but also a plump nest egg.

The wealth generated by housing in those decades did more than assure the owners a comfortable retirement. It powered the economy, paying for the education of children and grandchildren, keeping the cruise ships and golf courses full and the restaurants humming.

More than likely, that era is gone for good.

“There is no iron law that real estate must appreciate,’’ said Stan Humphries, chief economist for the real estate site Zillow. “All those theories advanced during the boom about why housing is special — that more people are choosing to spend more on housing, that more people are moving to the coasts, that we were running out of usable land — didn’t hold up.’’

Instead, Humphries and other economists say, housing values will only keep up with inflation. A home will return the money an owner puts in each month, but will not multiply the investment.

Dean Baker, codirector of the Center for Economic and Policy Research, estimates that it will take 20 years to recoup the $6 trillion of housing wealth that has been lost since 2005. After adjusting for inflation, values will never catch up.

Sunday, August 29, 2010

LOCAL NEWS: Mass. home sales drop in July for first time this year

The sales of Massachusetts single-family homes fell 26 percent in July, reversing a trend of 12 straight months of increases, the Warren Group reported this morning.

Earlier this year, a temporary federal tax credit for buyers helped give the housing market a lift --- thanks largely to the tax credit, June had the highest number of local monthly sales in four years as home buyers scrambled to take advantage of the tax credit before its expiration. But with the tax credit now mostly out of the picture, local sales fell sharply.

"It's disappointing to see such a big drop in sales," Warren Group chief executive Timothy M. Warren Jr said in a statement. "It appears the expiration of the home buyer tax credit hurt sales volume. Buyers aren't entering the market as aggressively as they were earlier this year. Whether this is a temporary dip due to the rush to qualify for the tax credit, or whether this is a sign of a declining market for the balance of the year is the big question in my mind."

(Under the original federal incentive program, first-time home buyers could qualify for tax credits of up to $8,000 and existing home owners who wanted to buy a new home could qualify for credits of up to $6,500. But there were conditions. Buyers had to have signed a sales contract by April 30 and to have completed the sale by June 30. An extension was later approved that pushed back the second deadline. Buyers now have until Sept. 30 to complete their purchases. The extension only allows people who already have signed contracts to finish at the later date, an AP story noted.)

Headquartered in Boston, the Warren Group tracks local real estate activity. The Massachusetts Association of Realtors also issued a separate monthly report on the local housing market this morning. Although it uses a slightly different method to process data than the Warren Group does, the results of the Realtors' report were roughly comparable to those of the Warren Group's.

One bright spot: Prices for single-family homes rose last month. In Massachusetts, the median price of single-family homes climbed 3 percent to $315,000 in July, up from $305,000 a year earlier, the Warren Group said; it was the second straight month of the year that the median price exceeded $300,000.

On a volume basis, 3,668 single-family Massachusetts homes sold in July, down from 4,967 a year earlier, the fewest number of sales in the month of July since 1990, the Warren Group said.

Bay State "condominium sales also dropped in July, decreasing 32 percent from a year earlier," the Warren Group said in its report. "A total of 1,484 condos sold in July, down from 2,185 a year ago."

The median selling price for a Massachusetts condo was $285,000 last month, up 2.7 percent from $277,500 a year earlier, the Warren Group said.

The report from the Massachusetts Association of Realtors included a statement from association president Kevin Sears.

“It is obvious at this point that the momentum from the tax credit has not been sustained through the middle of the summer,” Sears said. “While the market conditions still favor the buyer - with historically low interest rates, increasing inventory, and more affordable pricing- we may have to wait until the natural supply of buyers builds back up.”

To see the latest Warren Group data on single-family homes, please click here.

To read a press release from the Massachusetts Association of Realtors on July sales figures, please click here.

Boston Globe August 24, 2010

Earlier this year, a temporary federal tax credit for buyers helped give the housing market a lift --- thanks largely to the tax credit, June had the highest number of local monthly sales in four years as home buyers scrambled to take advantage of the tax credit before its expiration. But with the tax credit now mostly out of the picture, local sales fell sharply.

"It's disappointing to see such a big drop in sales," Warren Group chief executive Timothy M. Warren Jr said in a statement. "It appears the expiration of the home buyer tax credit hurt sales volume. Buyers aren't entering the market as aggressively as they were earlier this year. Whether this is a temporary dip due to the rush to qualify for the tax credit, or whether this is a sign of a declining market for the balance of the year is the big question in my mind."

(Under the original federal incentive program, first-time home buyers could qualify for tax credits of up to $8,000 and existing home owners who wanted to buy a new home could qualify for credits of up to $6,500. But there were conditions. Buyers had to have signed a sales contract by April 30 and to have completed the sale by June 30. An extension was later approved that pushed back the second deadline. Buyers now have until Sept. 30 to complete their purchases. The extension only allows people who already have signed contracts to finish at the later date, an AP story noted.)

Headquartered in Boston, the Warren Group tracks local real estate activity. The Massachusetts Association of Realtors also issued a separate monthly report on the local housing market this morning. Although it uses a slightly different method to process data than the Warren Group does, the results of the Realtors' report were roughly comparable to those of the Warren Group's.

One bright spot: Prices for single-family homes rose last month. In Massachusetts, the median price of single-family homes climbed 3 percent to $315,000 in July, up from $305,000 a year earlier, the Warren Group said; it was the second straight month of the year that the median price exceeded $300,000.

On a volume basis, 3,668 single-family Massachusetts homes sold in July, down from 4,967 a year earlier, the fewest number of sales in the month of July since 1990, the Warren Group said.

Bay State "condominium sales also dropped in July, decreasing 32 percent from a year earlier," the Warren Group said in its report. "A total of 1,484 condos sold in July, down from 2,185 a year ago."

The median selling price for a Massachusetts condo was $285,000 last month, up 2.7 percent from $277,500 a year earlier, the Warren Group said.

The report from the Massachusetts Association of Realtors included a statement from association president Kevin Sears.

“It is obvious at this point that the momentum from the tax credit has not been sustained through the middle of the summer,” Sears said. “While the market conditions still favor the buyer - with historically low interest rates, increasing inventory, and more affordable pricing- we may have to wait until the natural supply of buyers builds back up.”

To see the latest Warren Group data on single-family homes, please click here.

To read a press release from the Massachusetts Association of Realtors on July sales figures, please click here.

Boston Globe August 24, 2010

Saturday, August 28, 2010

TAXES & FKINANCE: Home values down, but tax bills rise

Struggling homeowners feel the pinch as Mass. communities try to make ends meet. Despite dropping home values, Massachusetts property tax bills continued to rise last year.

http://www.boston.com/news/local/massachusetts/graphics/08_22_10_property_tax/

Revenue-hungry cities and towns, looking for money to pay for new buildings and to maintain services, have continued to push up local taxes, often asking voters to approve property tax overrides even as real estate values drop further.

The double whammy of lower home values and higher taxes — a phenomenon that has hit Massachusetts homeowners for several years — frustrates taxpayers as they endure the rocky economy.

“There’s absolutely no way you can sell a house in Dedham for what it’s assessed at,’’ said Janet Gorman, who has lived in the town with her husband for about 30 years.

The couple, who own two single-family homes and rental property in town, sought a tax abatement on one of the rentals and got about $900 knocked off their tax bill.

“And is Dedham any different than any other town? Probably not,’’ Gorman said.

The average tax bill on a single-family home in fiscal 2010 increased about $140, a 3.3 percent increase, according to figures released this month by the state Department of Revenue. The average tax bill for a single-family home was $4,390.

The statewide home values, which have more than doubled since 2000, peaked in 2007 but dropped about 4.6 percent last year to an average of $373,702.

Taking a longer view, both taxes and home values have risen over the last decade. Since 2000, average property taxes on single-family homes in Massachusetts have increased about 64 percent.

State and local officials defend the tax increases, and lower values.

“Not only is the 3.3 increase the lowest in 20 years, but it also marks the first time in at least 20 years that the annual percentage increase has gone down for four consecutive years,’’ said Bob Bliss, spokesman for the Department of Revenue.

Local officials also point out that property assessments are a snapshot of values from a year or two ago.

Rick Henderson, the assistant director of assessing in Dedham, pointed out that assessed values for fiscal 2010 are based on a home’s worth on Jan. 1, 2009, which was determined by home sales in 2008 in that community. A home’s actual value — different from its assessed value — might have changed significantly over the last two years, he said.

“The taxes are high and I think everybody’s taxes are high,’’ said Jeanette Geller of Needham, who has filed for abatements at least three times in the 50 years she has lived in her split-level home. She recently won an abatement of nearly $400. Overall, property values dropped in 281 communities for the fiscal year that ended June 30. Hardest hit were Brockton, Revere,, Lynn, and Rockland, where values were clipped at least 14 percent.

“We still have a large number of foreclosures in the city, which impacts the values of homes,’’ when they sell at lower prices by lenders eager to get out of the real estate business, said Mayor Linda M. Balzotti of Brockton. This is the second cycle of foreclosures the city has endured, she said. The first was caused by sub-prime mortgages. This cycle largely stems from homeowners who have lost their jobs or are underemployed.

“We still haven’t quite leveled out yet, but I’m hopeful we will shortly,’’ she said.

Friday, August 27, 2010

MORTGAGE & FINANCE: Do Adjustable-Rate Mortgages Make Sense Now?

Although they’ve been much maligned, adjustable-rate mortgages make sense in a variety of circumstances.

Adjustable-rate mortgages (ARMs) get bad press. The poster child for irresponsible borrowing, they’re the mortgage industry’s bad boys. But ARMs can be excellent loans for thrifty borrowers.

Adjustable-rate mortgages (ARMs) get bad press. The poster child for irresponsible borrowing, they’re the mortgage industry’s bad boys. But ARMs can be excellent loans for thrifty borrowers.

How ARMs work

An ARM begins with a low introductory rate that remains fixed for a specified period. Upon expiration, the interest rate periodically adjusts based on an underlying index, which goes up or down. This contrasts sharply with a fixed-rate mortgage (FRM), where the monthly payment remains consistent.

The chief advantage of an ARM is that it allows you to save money in the early years. However, it can become dangerous because historically, declining rates don’t last more than approximately five years. Therefore, payments on a 15- or 30-year ARM will generally increase over time. A plan to refinance when the introductory period ends is a terrific idea—if you can pull it off. But if you can’t, and are unable to make increased monthly payments, you may lose your home.

This unpredictability makes an ARM inherently riskier than its fixed-rate counterpart. With mortgage rates at 7.5% or less for 185 of the past 210 years, it’s a reasonable risk—except if you’re living through a period like the late 1970s and early 1980s, when interest rates hit 17%.

Is an ARM right for you today?

An ARM may be right if:

1. You plan to refinance or sell within five to seven years.

Since an ARM’s introductory interest rate is lower than its fixed-rate counterpart, you’ll save money during the loan’s first few years. The most common ARMs are 3/1, 5/1, and 7/1. The first digit indicates the number of years the introductory rate remains fixed; the second, the frequency of rate adjustments. (A 3/1 ARM has a fixed rate for three years, then adjusts annually.) If you pay off your loan, refinance, or sell before the introductory rate expires, an ARM makes sense.

Example: You borrow $300,000 to buy an investment property that you’ll fix up and resell within two years. Your options are either a 3/1 ARM that opens at 3.5% or an FRM that’s locked in at 5.5%. The ARM’s monthly payment during the first three years: $1,347.13; the FRM’s payment: $1,703.37. During the ARM’s introductory period, you’d save $356.24 monthly (about $4,275 annually). During the first two years, the aggregate savings would be about $8,550—a sizeable sum.

2. You want to pay as little as possible.

Money saved on a mortgage payment is money in your pocket. If you don’t want to pay any more than is absolutely necessary in the early years, you’re a good ARM candidate. You’ll generally save money over a 30-year fixed loan for the first seven or eight years.

3. You want to aggressively pay down your mortgage.

According to Dave Donhoff, a financial advisor at Leverage Planners in Kirkland, Wash., “An

How ARMs work

An ARM begins with a low introductory rate that remains fixed for a specified period. Upon expiration, the interest rate periodically adjusts based on an underlying index, which goes up or down. This contrasts sharply with a fixed-rate mortgage (FRM), where the monthly payment remains consistent.

The chief advantage of an ARM is that it allows you to save money in the early years. However, it can become dangerous because historically, declining rates don’t last more than approximately five years. Therefore, payments on a 15- or 30-year ARM will generally increase over time. A plan to refinance when the introductory period ends is a terrific idea—if you can pull it off. But if you can’t, and are unable to make increased monthly payments, you may lose your home.

This unpredictability makes an ARM inherently riskier than its fixed-rate counterpart. With mortgage rates at 7.5% or less for 185 of the past 210 years, it’s a reasonable risk—except if you’re living through a period like the late 1970s and early 1980s, when interest rates hit 17%.

Is an ARM right for you today?

An ARM may be right if:

1. You plan to refinance or sell within five to seven years.

Since an ARM’s introductory interest rate is lower than its fixed-rate counterpart, you’ll save money during the loan’s first few years. The most common ARMs are 3/1, 5/1, and 7/1. The first digit indicates the number of years the introductory rate remains fixed; the second, the frequency of rate adjustments. (A 3/1 ARM has a fixed rate for three years, then adjusts annually.) If you pay off your loan, refinance, or sell before the introductory rate expires, an ARM makes sense.

Example: You borrow $300,000 to buy an investment property that you’ll fix up and resell within two years. Your options are either a 3/1 ARM that opens at 3.5% or an FRM that’s locked in at 5.5%. The ARM’s monthly payment during the first three years: $1,347.13; the FRM’s payment: $1,703.37. During the ARM’s introductory period, you’d save $356.24 monthly (about $4,275 annually). During the first two years, the aggregate savings would be about $8,550—a sizeable sum.

2. You want to pay as little as possible.

Money saved on a mortgage payment is money in your pocket. If you don’t want to pay any more than is absolutely necessary in the early years, you’re a good ARM candidate. You’ll generally save money over a 30-year fixed loan for the first seven or eight years.

3. You want to aggressively pay down your mortgage.

According to Dave Donhoff, a financial advisor at Leverage Planners in Kirkland, Wash., “An

Thursday, August 26, 2010

LANDSCAPING: Opinion: Green Lawns Out of Fashion

Diane Faulkner’s lawn was always causing her trouble. This Jacksonville, Fla., resident traveled frequently, and in her absence, her thirsty, fussy grass would go brown or otherwise run afoul of her neighborhood association’s rules. She hated returning home to a $50 fine, but the last straw was when her travels took her to rural Kenya. Immersed in local life, she’d wake up at dawn with the villagers to walk miles along a dried-up river toward a water source, then return with a few gallons for cooking and washing.

“That was their whole morning,” she says. As soon as she got on the plane back to America, she had a thought: “How many gallons of water do I waste on that stinking lawn?” And more broadly, why did she even have a lawn in the first place?

It’s a question a growing number of sweaty Americans are asking as they push (or ride) their lawnmowers in the August heat. While a field of green, closely cropped grass is the default landscape for a “nice” neighborhood, there’s no reason it has to be. And there are plenty of reasons it shouldn’t be—at least if we value the planet and our time.

21 million acres

Historians aren’t exactly sure why lawns became as closely tied to the American dream as homeownership itself. Perhaps early suburban sorts wished to mimic the look of British castle grounds (minus the sheep that were responsible for the close cropping). The fad spread, the lawn care industry grew, and now 21 million acres of the USA are covered with grasses that wouldn’t grow well here if left to their own devices.

The fight to maintain this unnatural state exacts a toll. “It’s essentially like pushing a boulder up a hill,” notes Ted Steinberg, an environmental historian at Case Western Reserve University and author of American Green: The Obsessive Quest for the Perfect Lawn.

According to Stephen Kress of the National Audubon Society, homeowners apply 78 million pounds of pesticides a year to lawns, often to kill “weeds” such as dandelions and clover, perhaps not noticing that these plants look just as green as grass when you mow them.

Mowing itself requires fuel, just like our cars, with a similar impact on the environment. And all these woes are before you even get to the issue of water. According to Kress, maintaining non-native plants requires 10,000 gallons of water per year per lawn, over and above rainwater. That water doesn’t just show up by itself; it requires energy to get to your hose. In California, for example, the energy required to treat and move water amounts to 19% of total electricity use in the state.

In short, lawns are incredibly inefficient, and not just from an environmental perspective. Maintenance requires time and money, which people usually claim are in short supply. According to the Bureau of Labor Statistics’ American Time Use Survey, the average father of school-aged kids spends 1.6 hours a week on lawn and garden care—more time than he spends on reading, talking, playing, or doing educational activities with his kids combined.

Shaming away a trend

For all these reasons, there’s a growing backlash against suburban seas of green. “The perfect lawn is in peril,” reports Steinberg. Big chunks of Canada have banned certain lawn pesticides. In the U.S., municipalities such as Los Angeles and Raleigh, N.C., regulate how many times a week homeowners can turn on the sprinklers.

That said, while rationing water during droughts has merit, I don’t think policymakers should start regulating lawns broadly. Deploying inspectors to count the square footage of grass vs. wild plants is a waste of resources when states are cutting teachers and cops. The best approach is for all of us to start thinking of lawns as a fashion—a fashion like wearing the feathers of rare birds in hats was once a fashion.

Fashions can change when enough people decide they are ridiculous or wasteful. Few parents would light a cigarette at a playground anymore, even if it’s not illegal, and we should start treating the presence of a vast, green, cropped grass lawn in the middle of summer the same way: as a weird and antisocial thing.

Certainly, there are options.

“You don’t have to trade off the lawn for some hideous alternative,” notes Penny Lewis, executive director of the Ecological Landscaping Association. First, ask “how much lawn do you have and how much do you really need?”

Some homeowners keep a small patch of grass around the house and turn parts of the lawn into a meadow that attracts birds and butterflies. Others simply swear off pesticides and let the grass go dormant in the summer.

Faulkner, on the other hand, went all-in. She redid her lawn with rocks and hearty plants such as Confederate Jasmine, arranged to look like an English garden. Because all her plants grow well in Florida, they require no upkeep. “I don’t have to mow, I don’t have to water, I don’t have to trim,” she reports. Her water bill has gone from $80-$90/month to $20.

Her only lawn headache now? Figuring out what to do with the time and money she’s saving—a problem let’s hope more homeowners have soon.

Laura Vanderkam, author of 168 Hours: You Have More Time Than You Think, is a member of USA TODAY’s Board of Contributors. (c) Copyright 2010 USA TODAY, a division of Gannett Co. Inc.

Source: USA TODAY

Publication date: 2010-08-17

Read more: http://www.houselogic.com/news/articles/opinion-green-lawns-out-fashion/#ixzz0x3neMWlB

“That was their whole morning,” she says. As soon as she got on the plane back to America, she had a thought: “How many gallons of water do I waste on that stinking lawn?” And more broadly, why did she even have a lawn in the first place?

It’s a question a growing number of sweaty Americans are asking as they push (or ride) their lawnmowers in the August heat. While a field of green, closely cropped grass is the default landscape for a “nice” neighborhood, there’s no reason it has to be. And there are plenty of reasons it shouldn’t be—at least if we value the planet and our time.

21 million acres

Historians aren’t exactly sure why lawns became as closely tied to the American dream as homeownership itself. Perhaps early suburban sorts wished to mimic the look of British castle grounds (minus the sheep that were responsible for the close cropping). The fad spread, the lawn care industry grew, and now 21 million acres of the USA are covered with grasses that wouldn’t grow well here if left to their own devices.

The fight to maintain this unnatural state exacts a toll. “It’s essentially like pushing a boulder up a hill,” notes Ted Steinberg, an environmental historian at Case Western Reserve University and author of American Green: The Obsessive Quest for the Perfect Lawn.

According to Stephen Kress of the National Audubon Society, homeowners apply 78 million pounds of pesticides a year to lawns, often to kill “weeds” such as dandelions and clover, perhaps not noticing that these plants look just as green as grass when you mow them.

Mowing itself requires fuel, just like our cars, with a similar impact on the environment. And all these woes are before you even get to the issue of water. According to Kress, maintaining non-native plants requires 10,000 gallons of water per year per lawn, over and above rainwater. That water doesn’t just show up by itself; it requires energy to get to your hose. In California, for example, the energy required to treat and move water amounts to 19% of total electricity use in the state.

In short, lawns are incredibly inefficient, and not just from an environmental perspective. Maintenance requires time and money, which people usually claim are in short supply. According to the Bureau of Labor Statistics’ American Time Use Survey, the average father of school-aged kids spends 1.6 hours a week on lawn and garden care—more time than he spends on reading, talking, playing, or doing educational activities with his kids combined.

Shaming away a trend

For all these reasons, there’s a growing backlash against suburban seas of green. “The perfect lawn is in peril,” reports Steinberg. Big chunks of Canada have banned certain lawn pesticides. In the U.S., municipalities such as Los Angeles and Raleigh, N.C., regulate how many times a week homeowners can turn on the sprinklers.

That said, while rationing water during droughts has merit, I don’t think policymakers should start regulating lawns broadly. Deploying inspectors to count the square footage of grass vs. wild plants is a waste of resources when states are cutting teachers and cops. The best approach is for all of us to start thinking of lawns as a fashion—a fashion like wearing the feathers of rare birds in hats was once a fashion.

Fashions can change when enough people decide they are ridiculous or wasteful. Few parents would light a cigarette at a playground anymore, even if it’s not illegal, and we should start treating the presence of a vast, green, cropped grass lawn in the middle of summer the same way: as a weird and antisocial thing.

Certainly, there are options.

“You don’t have to trade off the lawn for some hideous alternative,” notes Penny Lewis, executive director of the Ecological Landscaping Association. First, ask “how much lawn do you have and how much do you really need?”

Some homeowners keep a small patch of grass around the house and turn parts of the lawn into a meadow that attracts birds and butterflies. Others simply swear off pesticides and let the grass go dormant in the summer.

Faulkner, on the other hand, went all-in. She redid her lawn with rocks and hearty plants such as Confederate Jasmine, arranged to look like an English garden. Because all her plants grow well in Florida, they require no upkeep. “I don’t have to mow, I don’t have to water, I don’t have to trim,” she reports. Her water bill has gone from $80-$90/month to $20.

Her only lawn headache now? Figuring out what to do with the time and money she’s saving—a problem let’s hope more homeowners have soon.

Laura Vanderkam, author of 168 Hours: You Have More Time Than You Think, is a member of USA TODAY’s Board of Contributors. (c) Copyright 2010 USA TODAY, a division of Gannett Co. Inc.

Source: USA TODAY

Publication date: 2010-08-17

Read more: http://www.houselogic.com/news/articles/opinion-green-lawns-out-fashion/#ixzz0x3neMWlB

Wednesday, August 25, 2010

SAVING ENERGY: Homeowners Aware But Not Taking Action With Green Alternatives

While 59% of Americans considered green alternatives for their home improvement projects, only 19% were motivated by tax credits for energy-efficiency products, according to data collected by ServiceMagic, a matching service for finding contractors.

The company, which compiled the data from 1.6 million service requests and a survey of 1,200 homeowners and 500 service professionals, said when homeowners did go green, they focused largely on window upgrades for the home.

Eighty three percent of survey respondents invested in windows for energy reasons with cost saving from increased energy efficiency being the top motivation. Top reasons homeowners didn’t request energy-efficient window systems were that green products were too expensive, the tax credit did not justify the additional expense, or they weren’t aware of the tax credit.

Beyond window projects, going green isn’t in demand

For homeowners who didn’t consider green alternatives:

50% weren’t aware of the green options.

27% didn’t like the green product choices.

16% found the cost of green products outweighed the benefits.

Fewer than 10% requested green or energy-efficient alternatives for their home improvement projects, as reported by 62% of service professionals.

Houselogic.com August 12, 2010Source: ServiceMagic

Read more: http://www.houselogic.com/news/articles/homeowners-aware-but-not-taking-action-green-alternatives/#ixzz0x3mpa6EE

The company, which compiled the data from 1.6 million service requests and a survey of 1,200 homeowners and 500 service professionals, said when homeowners did go green, they focused largely on window upgrades for the home.

Eighty three percent of survey respondents invested in windows for energy reasons with cost saving from increased energy efficiency being the top motivation. Top reasons homeowners didn’t request energy-efficient window systems were that green products were too expensive, the tax credit did not justify the additional expense, or they weren’t aware of the tax credit.

Beyond window projects, going green isn’t in demand

For homeowners who didn’t consider green alternatives:

50% weren’t aware of the green options.

27% didn’t like the green product choices.

16% found the cost of green products outweighed the benefits.

Fewer than 10% requested green or energy-efficient alternatives for their home improvement projects, as reported by 62% of service professionals.

Houselogic.com August 12, 2010Source: ServiceMagic

Read more: http://www.houselogic.com/news/articles/homeowners-aware-but-not-taking-action-green-alternatives/#ixzz0x3mpa6EE

Tuesday, August 24, 2010

SAVING ENERGY: Survey Shows Many are Clueless on How to Save Energy

The largest group, nearly 20%, cited turning off lights as the best approach—an action that affects energy budgets relatively little. Very few cited buying decisions that experts say would cut U.S. energy consumption dramatically, such as more efficient cars (cited by only 2.8%), more efficient appliances (cited by 3.2%, or weatherizing homes (cited by 2.1%).

Previous researchers have concluded that households could reduce energy consumption some 30% by making such choices—all without waiting for new technologies, making big economic sacrifices or losing their sense of well-being.

Lead author Shahzeen Attari, a postdoctoral fellow at Columbia University’s Earth Institute and the university’s Center for Research on Environmental Decisions, said multiple factors probably are driving the misperceptions.

“When people think of themselves, they may tend to think of what they can do that is cheap and easy at the moment,” she said. On a broader scale, she said, even after years of research, scientists, government, industry, and environmental groups may have “failed to communicate” what they know about the potential of investments in technology; instead, they have funded recycling drives and encouraged actions like turning off lights.

In general, the people surveyed tend to believe in what Attari calls curtailment. “That is, keeping the same behavior, but doing less of it,” she said. “But switching to efficient technologies generally allows you to maintain your behavior, and save a great deal more energy,” she said. She cited high-efficiency light bulbs, which can be kept on all the time, and still save more than minimizing the use of low-efficiency ones.

Monday, August 23, 2010

A big reason for owning a vacation home is rest and relaxation, but it’s not all fun and games. Opening and closing a vacation home takes time and money. Plan to spend a day before the season starts to open your vacation home, and another day at season’s end to close it down.

Specific tasks, such as draining off pipes or turning on utilities, will depend on climate, as well as when and how the vacation home is used. A beach cottage has different requirements than a mountain cabin. If you don’t live nearby or don’t want to do the work yourself, be sure to budget for a property manager or local caretaker.

Opening a vacation home

When it’s time to visit your vacation home for the first time, or start renting it out for the season, you’ll need to get it ready. A ski chalet might require you to shovel snow and chop firewood, while a summer retreat by the shore might call for cleaning patio furniture and staining the deck.

Much depends on how well the house is maintained throughout the year. Opening your vacation home could be as easy as stocking the pantry, or if the house was neglected in the offseason, you could have multiple repairs on your hands.

A well-maintained vacation home shouldn’t take more than a day to get in shape for the season, assuming no major repairs are needed.

Here are some typical opening chores:

Turn on utilities

Clean and stock kitchen and bathrooms

Look for evidence of plumbing and roof leaks

Cut lawn and trim shrubs/trees

Clear walkways and driveway

Set up outdoor furniture

Change lightbulbs and smoke detector batteries

Replace furnace filters

Check for signs of pest infestation

Closing a vacation home

Closing a vacation home also takes about a day to complete. The emphasis should be on safeguarding your home against the elements as well as fire risks.

Here are some common closing tasks:

Turn off nonessential utilities

Secure all windows and doors

Turn on alarm system

Close storm shutters

Dispose of trash and perishable foods

Adjust furnace settings for climate

Bring in outdoor furniture

Unplug appliances and electronics

Drain water lines to prevent freezing (in cold climates)

Request mail-forwarding service

To deter vandalism and theft, consider installing a home security system. You can also put in automatic indoor lights that turn on at dusk or outside flood lights that are motion-activated.

Sunday, August 22, 2010

Nothing lasts forever, including the pipes inside your house. Over the decades, the tubing gradually corrodes, rusts, and decays. Unless you replace plumbing, you’re eventually going to get leaks—and possibly a flood of water or raw sewage into your home that causes thousands of dollars in damage to your building and belongings.

But is a plumbing disaster imminent or just a concern for the distant future? Replacing old pipes in a 1,500 square foot, two-bathroom home costs $4,000 to $10,000, and requires cutting open walls and floors, so you certainly don’t want to do the job before it’s necessary. Here’s how to assess your plumbing system and know when it’s time for replacement.

Know your pipes

The type of plumbing in your house determines how long you can expect it to last. So review the home inspection report you got when you bought your home to see what kind of pipes you have—or bring in a trusted plumber to do a free inspection of your plumbing system.

Your pipes’ lifespan

Type Material Typical lifespan

Supply pipes (under constant pressure and therefore most likely to cause water damage when they leak)

Brass 80-100 yrs

Copper 70-80 yrs

Galvanized steel 80-100 yrs

Drain lines Cast iron 80-100 yrs

Polyvinyl chloride 25-40 yrs

(known as PVC)

If your pipes are older than these guidelines, it doesn’t necessarily mean they need to be replaced. Well-maintained pipes may last longer, and poorly maintained ones or those in areas with hard water (meaning it has high mineral content), may fail sooner, says Passaic, N.J., plumber Joseph Gove, who supplied the lifespan estimates.

So, no matter what kind of pipes you have and how old they are, you need to keep an eye on them.

Remove lead and polybutylene

There are two other types of water supply pipe that should be removed immediately no matter how old they are.

Lead pipes, used in the early 1900s, have a life expectancy of 100 years, but they can leach lead into your drinking water, a serious health hazard.

Polybutylene pipes, used from the 1970s through the 1990s, are extremely prone to breakage.

Watch for signs of trouble

If your house is more than about 60 years old, make it an annual ritual to look at any exposed pipe—in basements, crawlspaces, and utility rooms—for telltale signs of trouble. Check the tubing for discoloration, stains, dimpling, pimples, or flaking, which are all indications of corrosion. If you find irregularities, bring in a plumber to do an inspection.

Saturday, August 21, 2010

HOME DESIGN: Old house, new paint job has Chatham residents all abuzz

CHATHAM — First, it was the sharks. Now, some say, a neon nuisance is threatening the subtle beauty of this quaint seaside town.

When a historic house in Chatham’s Old Village was transformed this month from traditional Yankee white to a fluorescent palette of green, lime, and citrus yellow, some longtime residents blanched at the sight. But weeks later, others have begun quietly cheering the curious color scheme for its ability to turn heads, and open wallets, in Chatham.

When a historic house in Chatham’s Old Village was transformed this month from traditional Yankee white to a fluorescent palette of green, lime, and citrus yellow, some longtime residents blanched at the sight. But weeks later, others have begun quietly cheering the curious color scheme for its ability to turn heads, and open wallets, in Chatham.

“It’s been great for business,’’ said Suzanne J. Nethercote, an artist who sells her work out of the Old Village Co-Op Art Gallery, which operates out of the first floor of the historic home. “We’ve had many people come in here because they’re interested in why it was painted this way and leave with a painting.’’

Although the couple who own the house deny it, many Chatham residents see the new look as the latest salvo in a contentious drama that has played out over the last three years between the building’s owners and the town.

“Beauty, like motive, is in the eye of the beholder,’’ Bill Riley, the couples’ lawyer, said yesterday. “I think what’s really at work is we conform because we want approval of our neighbors. And if your neighbors reject you, the pressure to conform is really relieved, and you’re free to make a decision that pleases only you.’’

The house is set among white and weather-grayed shingles the Cape is known for. Hilary and Tina Foulkes, who live in Germany, bought the property in 2005 with hopes of renovating it for use as a summer getaway. Their requests, which included moving the house 6 feet back from Main Street, a widow’s walk on the roof, and an addition to the south-side of the building, were denied several times by committees and councils at every step.

Tensions mounted.

“I remember one hearing it was a complete circus,’’ Riley said. “We went into the hearing, and the room was packed, every seat was taken. It seemed the world was going to end if we didn’t leave the building exactly as it was.’’

The house, a Greek-revival building that towers over its neighbors, is a beloved symbol of the town, said local resident Carol Pacun, who said the paint job is “bizarre at best.’’

“I remember there was a lot of concern over whether the historic aspect of the house would be harmed,’’ she said. “It was very distressing.’’

Maintaining the historic integrity of the village is very important to many longtime Chatham residents.

“It’s been great for business,’’ said Suzanne J. Nethercote, an artist who sells her work out of the Old Village Co-Op Art Gallery, which operates out of the first floor of the historic home. “We’ve had many people come in here because they’re interested in why it was painted this way and leave with a painting.’’

Although the couple who own the house deny it, many Chatham residents see the new look as the latest salvo in a contentious drama that has played out over the last three years between the building’s owners and the town.

“Beauty, like motive, is in the eye of the beholder,’’ Bill Riley, the couples’ lawyer, said yesterday. “I think what’s really at work is we conform because we want approval of our neighbors. And if your neighbors reject you, the pressure to conform is really relieved, and you’re free to make a decision that pleases only you.’’

The house is set among white and weather-grayed shingles the Cape is known for. Hilary and Tina Foulkes, who live in Germany, bought the property in 2005 with hopes of renovating it for use as a summer getaway. Their requests, which included moving the house 6 feet back from Main Street, a widow’s walk on the roof, and an addition to the south-side of the building, were denied several times by committees and councils at every step.

Tensions mounted.

“I remember one hearing it was a complete circus,’’ Riley said. “We went into the hearing, and the room was packed, every seat was taken. It seemed the world was going to end if we didn’t leave the building exactly as it was.’’

The house, a Greek-revival building that towers over its neighbors, is a beloved symbol of the town, said local resident Carol Pacun, who said the paint job is “bizarre at best.’’

“I remember there was a lot of concern over whether the historic aspect of the house would be harmed,’’ she said. “It was very distressing.’’

Maintaining the historic integrity of the village is very important to many longtime Chatham residents.

Friday, August 20, 2010

BOSTON NEIGHBORHOODS: Revival on tap for Hub channel: $11m plan turns Fort Point into a social hot spot

Boston’s Fort Point Channel, for decades a polluted workhorse of industry, is about to undergo a dramatic transformation to a recreational and social playground that could host floating restaurants and music shows, kayak rentals and fishing charters.

This fall, major property owners along the channel will lay the groundwork for its renaissance with new public docks that will increase access to the milelong waterway, advancing the city’s vision of a civic space akin to the Boston Common or the Rose Fitzgerald Kennedy Greenway.

An $11 million plan for improvements to the channel is modeled, in part, on waterfronts in Chicago, Seattle, and other cities where museums, outdoor dining, and public events draw crowds to their shorelines.

The catalyst for the burst of activity in Boston is a law signed earlier this month by Governor Deval Patrick that essentially rezones the channel for recreational use, allowing installation of docks and other floating structures that were once banned to protect commercial navigation.

“These changes will allow us to take an urban waterway and activate it in ways that have been very successful in other cities,’’ said James Rooney, head of the nearby convention center and president of Friends of the Fort Point Channel, a civic group involved in the channel restoration.

Most of the boat ramps, taxi stations and docks will be built by commercial property owners who are required by their environmental permits to improve public access and amenities to their waterfronts.

Funds for many other improvements, such as floating art barges and water festivals, will be raised from fees charged to firms planning future building projects in the area.

New developments are moving slowly in the down economy, so it may take several years before new attractions are built. The shuttered Boston Tea Party Museum, for example, is still raising money to complete renovations and reopen facilities closed after being struck by lightning in 2001.

Another wave of improvements will probably result from the eventual redevelopment of the US Postal Service mail facility, which is planning to relocate to South Boston. But that project, too, has also been slowed by the recession.

Still, the new access points to begin construction this fall will open the channel to an array of possibilities, including floating restaurants and cafes, fountains, model boat racing, and other attractions included in a plan City Hall has for the area.

“I’ve always seen this area as a great opportunity for rowing and other events on the water,’’ Mayor Thomas M. Menino said in an interview. “Right now, it’s really just dead, unused space. But the improvements in access will help us open it up and plan for the future of that whole area.’’

Already Boston Properties has built a 60-foot ramp to a dock that will provide temporary docking service for visiting boaters behind the 32-story tower it is building at the corner of Congress Street and Atlantic Avenue. The tower will have an expansive public plaza on the channel to eventually include a new tour service and concierge desk that will provide information on waterfront attractions.

Further up the channel, Procter & Gamble Co., which owns Gillette and its sprawling headquarters in South Boston, will begin construction this fall on a 60-foot dock in an area that will be dedicated to canoeing and kayaking. City officials are also urging Procter & Gamble to provide free public parking on its property, a request the firm is considering.

This fall, major property owners along the channel will lay the groundwork for its renaissance with new public docks that will increase access to the milelong waterway, advancing the city’s vision of a civic space akin to the Boston Common or the Rose Fitzgerald Kennedy Greenway.

An $11 million plan for improvements to the channel is modeled, in part, on waterfronts in Chicago, Seattle, and other cities where museums, outdoor dining, and public events draw crowds to their shorelines.

The catalyst for the burst of activity in Boston is a law signed earlier this month by Governor Deval Patrick that essentially rezones the channel for recreational use, allowing installation of docks and other floating structures that were once banned to protect commercial navigation.

“These changes will allow us to take an urban waterway and activate it in ways that have been very successful in other cities,’’ said James Rooney, head of the nearby convention center and president of Friends of the Fort Point Channel, a civic group involved in the channel restoration.

Most of the boat ramps, taxi stations and docks will be built by commercial property owners who are required by their environmental permits to improve public access and amenities to their waterfronts.

Funds for many other improvements, such as floating art barges and water festivals, will be raised from fees charged to firms planning future building projects in the area.

New developments are moving slowly in the down economy, so it may take several years before new attractions are built. The shuttered Boston Tea Party Museum, for example, is still raising money to complete renovations and reopen facilities closed after being struck by lightning in 2001.

Another wave of improvements will probably result from the eventual redevelopment of the US Postal Service mail facility, which is planning to relocate to South Boston. But that project, too, has also been slowed by the recession.

Still, the new access points to begin construction this fall will open the channel to an array of possibilities, including floating restaurants and cafes, fountains, model boat racing, and other attractions included in a plan City Hall has for the area.

“I’ve always seen this area as a great opportunity for rowing and other events on the water,’’ Mayor Thomas M. Menino said in an interview. “Right now, it’s really just dead, unused space. But the improvements in access will help us open it up and plan for the future of that whole area.’’

Already Boston Properties has built a 60-foot ramp to a dock that will provide temporary docking service for visiting boaters behind the 32-story tower it is building at the corner of Congress Street and Atlantic Avenue. The tower will have an expansive public plaza on the channel to eventually include a new tour service and concierge desk that will provide information on waterfront attractions.

Further up the channel, Procter & Gamble Co., which owns Gillette and its sprawling headquarters in South Boston, will begin construction this fall on a 60-foot dock in an area that will be dedicated to canoeing and kayaking. City officials are also urging Procter & Gamble to provide free public parking on its property, a request the firm is considering.

Thursday, August 19, 2010

MORTGAGE & FINANCE: Low mortgage rates make refinancing rather tempting

WASHINGTON — With mortgage interest rates setting record lows almost every week for more than two months, two questions naturally come to mind: How low can they go? And should I refinance — again?

Last week rates fell to levels that many people in the mortgage business thought they would never see. Freddie Mac reported Thursday that the average rate on a 30-year, fixed-rate loan was 4.44 percent, with 0.7 of a point in prepaid interest. (One point equals 1 percent of the loan amount.) Loans fixed for 15 years also hit a record low, 3.92 percent, with 0.6 of a point, on average.

Loans that are fixed for five years and then convert to annual interest-rate adjustments averaged 3.56 percent last week. One-year adjustables averaged 3.53 percent. Both charged an average of 0.7 of a point, according to Freddie Mac.

Frank Nothaft, Freddie Mac’s chief economist, said in a report issued last week: “The ability to lock in a principal and interest payment at below 5 percent for 30 years is rare enough. The fact that a 30-year, fixed-rate mortgage can be obtained for 4.5 percent, or a 15-year mortgage for 4 percent is an amazing opportunity for borrowers.’’

However, Greg McBride, senior financial analyst for Bankrate.com, said: “The pool of refi candidates has been dwindling because we have been below 5 1/2 percent for the past year. People may not want to invest the time and money in another go-round.’’

He added that, in markets where values are still declining, an appraisal that was high enough to support a refinance just eight months ago may not be at the same value now.

Homeowners should not assume that they wouldn’t qualify for a new loan, said Malcolm Hollensteiner, mid-Atlantic regional manager for PNC Mortgage.

“There’s a large percentage of the population that doesn’t feel they are eligible to refinance, but they are,’’ he said. “Until you go through the process, you don’t know if you do.’’

Rates are higher on jumbo loans for amounts greater than $729,750, which are too big to be eligible for purchase by Freddie Mac and Fannie Mae. But the spread between jumbos and smaller “conforming’’ loans has narrowed significantly this year, Hollensteiner said. He said borrowers have to pay interest rates of about half to three-quarters of a percentage point more for jumbos. A year ago the difference was about 1 to 1.5 percentage points.

Refinancings now constitute most of the mortgage market, accounting for 78 percent of all loan applications nationwide, the Mortgage Bankers Association reported this week. And many refinancers are taking the opportunity to move into shorter-term loans that carry a lower interest rate and build equity faster. That’s a particularly attractive option for people who hope to pay off their mortgage before retirement.

Economists at Freddie Mac reported last week that during the second quarter, 30 percent of borrowers who were refinancing out of 30-year, fixed-rate loans chose new fixed-rate loans lasting 15 or 20 years. That’s the highest level of term-shortening the company has seen in six years. But other borrowers, Hollensteiner said, “are more focused on lowering their monthly payments.’’ And a significant number are pulling out equity when they refinance, using the cash to pay for home improvements or education expenses, he said.

Unless you had a high rate to begin with (say 6.5 percent or more) switching to a shorter-term loan boosts the monthly payment but can save a lot of money over the duration of the loan. For a $200,000 loan, switching from a 30-year rate at 5 percent to a 15-year loan fixed at 3.92 percent would increase the monthly payment by about $400 per month. But by paying off the loan in half the time, you would save about $122,000.

But refinancing isn’t free, even if the lender offers to roll over the expense into your new loan balance. Hollensteiner said nonrecoverable closing costs, such as loan application fees or government recordation fees, are typically about 1 percent of the loan amount. Depending on variables such as the day of the month you close on the new loan, you could have to come up with a similar amount in expenses that you will recover after closing, say from a disbursement from your old escrow account. These expenses include property tax payments and daily interest expenses.

“It’s all a wash, but it’s still money you need to have at closing,’’ Hollensteiner said.

Might rates go even lower? Perhaps, but probably not by much, according to Celia Chen, senior director at Moody’s Analytics. “I don’t think they’re going to fall much further; they’re at a record right now,’’ she said. “And even at this low rate, it doesn’t seem to be doing much to support the housing market.’’

And though it’s remarkable to note how many weeks in a row Freddie Mac’s mortgage rate series has marked record lows (seven times in the past eight weeks), the week-to-week changes have been tiny, usually only one hundredth or two hundredths of a percentage point at a time. Chen said she expects mortgage interest trends to remain “fairly stable at a low rate.’’

Elizabeth Razzi Washington Post August 15, 2010

Last week rates fell to levels that many people in the mortgage business thought they would never see. Freddie Mac reported Thursday that the average rate on a 30-year, fixed-rate loan was 4.44 percent, with 0.7 of a point in prepaid interest. (One point equals 1 percent of the loan amount.) Loans fixed for 15 years also hit a record low, 3.92 percent, with 0.6 of a point, on average.

Loans that are fixed for five years and then convert to annual interest-rate adjustments averaged 3.56 percent last week. One-year adjustables averaged 3.53 percent. Both charged an average of 0.7 of a point, according to Freddie Mac.

Frank Nothaft, Freddie Mac’s chief economist, said in a report issued last week: “The ability to lock in a principal and interest payment at below 5 percent for 30 years is rare enough. The fact that a 30-year, fixed-rate mortgage can be obtained for 4.5 percent, or a 15-year mortgage for 4 percent is an amazing opportunity for borrowers.’’

However, Greg McBride, senior financial analyst for Bankrate.com, said: “The pool of refi candidates has been dwindling because we have been below 5 1/2 percent for the past year. People may not want to invest the time and money in another go-round.’’

He added that, in markets where values are still declining, an appraisal that was high enough to support a refinance just eight months ago may not be at the same value now.

Homeowners should not assume that they wouldn’t qualify for a new loan, said Malcolm Hollensteiner, mid-Atlantic regional manager for PNC Mortgage.

“There’s a large percentage of the population that doesn’t feel they are eligible to refinance, but they are,’’ he said. “Until you go through the process, you don’t know if you do.’’

Rates are higher on jumbo loans for amounts greater than $729,750, which are too big to be eligible for purchase by Freddie Mac and Fannie Mae. But the spread between jumbos and smaller “conforming’’ loans has narrowed significantly this year, Hollensteiner said. He said borrowers have to pay interest rates of about half to three-quarters of a percentage point more for jumbos. A year ago the difference was about 1 to 1.5 percentage points.

Refinancings now constitute most of the mortgage market, accounting for 78 percent of all loan applications nationwide, the Mortgage Bankers Association reported this week. And many refinancers are taking the opportunity to move into shorter-term loans that carry a lower interest rate and build equity faster. That’s a particularly attractive option for people who hope to pay off their mortgage before retirement.

Economists at Freddie Mac reported last week that during the second quarter, 30 percent of borrowers who were refinancing out of 30-year, fixed-rate loans chose new fixed-rate loans lasting 15 or 20 years. That’s the highest level of term-shortening the company has seen in six years. But other borrowers, Hollensteiner said, “are more focused on lowering their monthly payments.’’ And a significant number are pulling out equity when they refinance, using the cash to pay for home improvements or education expenses, he said.

Unless you had a high rate to begin with (say 6.5 percent or more) switching to a shorter-term loan boosts the monthly payment but can save a lot of money over the duration of the loan. For a $200,000 loan, switching from a 30-year rate at 5 percent to a 15-year loan fixed at 3.92 percent would increase the monthly payment by about $400 per month. But by paying off the loan in half the time, you would save about $122,000.

But refinancing isn’t free, even if the lender offers to roll over the expense into your new loan balance. Hollensteiner said nonrecoverable closing costs, such as loan application fees or government recordation fees, are typically about 1 percent of the loan amount. Depending on variables such as the day of the month you close on the new loan, you could have to come up with a similar amount in expenses that you will recover after closing, say from a disbursement from your old escrow account. These expenses include property tax payments and daily interest expenses.

“It’s all a wash, but it’s still money you need to have at closing,’’ Hollensteiner said.

Might rates go even lower? Perhaps, but probably not by much, according to Celia Chen, senior director at Moody’s Analytics. “I don’t think they’re going to fall much further; they’re at a record right now,’’ she said. “And even at this low rate, it doesn’t seem to be doing much to support the housing market.’’

And though it’s remarkable to note how many weeks in a row Freddie Mac’s mortgage rate series has marked record lows (seven times in the past eight weeks), the week-to-week changes have been tiny, usually only one hundredth or two hundredths of a percentage point at a time. Chen said she expects mortgage interest trends to remain “fairly stable at a low rate.’’

Elizabeth Razzi Washington Post August 15, 2010

Wednesday, August 18, 2010

LOCAL NEWS: Longwood Towers up for rent

BROOKLINE — It is back to the future at Longwood Towers.

Five years after a developer purchased the stately apartment complex for about $110 million, with plans to sell the 277 apartments in three buildings as condos, a new owner has temporarily scrapped plans to complete the final phase and instead put newly renovated units up for rent.

The historic complex, a towering symbol of Old World style that is steps from the Longwood Medical Area, has gone through a tortured evolution of ownership and complications since an Atlanta developer, Radco Cos. and its investment partner Arcapita Inc. launched an ambitious $30 million renovation project in 2005, just as the housing market began to decline.

The historic complex, a towering symbol of Old World style that is steps from the Longwood Medical Area, has gone through a tortured evolution of ownership and complications since an Atlanta developer, Radco Cos. and its investment partner Arcapita Inc. launched an ambitious $30 million renovation project in 2005, just as the housing market began to decline.

Improvements in the 1920s buildings included upgraded kitchens, bathrooms, and hallways, as well as more elaborate plans, soon discarded, to create a driving range, cigar bar, and cinema.

In 2008, as the housing market continued to slow, mortgage holder IStar Financial Inc. seized the Tudor-style complex from the financially struggling developers and completed two of the three 11-story towers on its own. A year later, IStar surprised the real estate industry by announcing an auction of 40 units at discount prices, in hopes of spurring sales and unloading inventory.

The values of the condos, originally slated to sell for $600 to $700 a square foot, fell to about $475 a square foot. The units quickly sold out in the first two towers.

Real estate executive Edward Zuker then purchased the last remaining tower, an 87-unit building, for $18 million and invested about $10 million in renovations, currently underway.

Zuker, chief executive of Brookline-based Chestnut Hill Realty, said he originally planned to sell the units as condos but recently decided to change his strategy, rent them out for between $2,700 and $10,000 a month, and wait for the market to turn.

Five years after a developer purchased the stately apartment complex for about $110 million, with plans to sell the 277 apartments in three buildings as condos, a new owner has temporarily scrapped plans to complete the final phase and instead put newly renovated units up for rent.

Improvements in the 1920s buildings included upgraded kitchens, bathrooms, and hallways, as well as more elaborate plans, soon discarded, to create a driving range, cigar bar, and cinema.

In 2008, as the housing market continued to slow, mortgage holder IStar Financial Inc. seized the Tudor-style complex from the financially struggling developers and completed two of the three 11-story towers on its own. A year later, IStar surprised the real estate industry by announcing an auction of 40 units at discount prices, in hopes of spurring sales and unloading inventory.

The values of the condos, originally slated to sell for $600 to $700 a square foot, fell to about $475 a square foot. The units quickly sold out in the first two towers.

Real estate executive Edward Zuker then purchased the last remaining tower, an 87-unit building, for $18 million and invested about $10 million in renovations, currently underway.

Zuker, chief executive of Brookline-based Chestnut Hill Realty, said he originally planned to sell the units as condos but recently decided to change his strategy, rent them out for between $2,700 and $10,000 a month, and wait for the market to turn.

Tuesday, August 17, 2010

FINANCE NEWS: Fewer homeowners are ‘underwater’

NEW YORK — The percentage of homeowners who owe more than their properties are worth declined in the second quarter as tax credits boosted prices in California and foreclosures surged, the real estate data provider Zillow.com said yesterday.

The Seattle firm found that 21.5 percent of homeowners were “underwater’’ on their mortgages, down from 23.3 percent in the first quarter and 23 percent a year earlier.

The decline came as property prices in California were bolstered by state and federal benefits for buyers, Zillow said. Prices climbed from a year earlier in 28 percent of the markets tracked in California, the most populous state. They gained 5.5 percent in the Los Angeles area, 5.9 percent in San Francisco, and 7.3 percent in San Diego.

“The double tax credits for some California homebuyers have certainly stimulated housing demand there and are partly responsible for the rapid — and likely unsustainable — rates of appreciation in many markets across the state,’’ Stan Humphries, chief economist at Zillow, said in a statement.

Home buyers seeking the federal benefit had to sign contracts by April 30 to qualify for a tax credit of up to $8,000 and have until Sept. 30 to complete their purchases. In California, buyers could qualify for a credit of up to $10,000 under a program that began May 1.

Foreclosures reached a high in June, with more than one of every 1,000 homes taken over by lenders, Zillow said. The number of properties receiving a notice of default, auction, or bank seizure climbed in three-quarters of US metropolitan areas in the first half of 2010, Irvine, Calif.-based RealtyTrac Inc. said on July 29

Associated Press August 10, 2010

The Seattle firm found that 21.5 percent of homeowners were “underwater’’ on their mortgages, down from 23.3 percent in the first quarter and 23 percent a year earlier.

The decline came as property prices in California were bolstered by state and federal benefits for buyers, Zillow said. Prices climbed from a year earlier in 28 percent of the markets tracked in California, the most populous state. They gained 5.5 percent in the Los Angeles area, 5.9 percent in San Francisco, and 7.3 percent in San Diego.

“The double tax credits for some California homebuyers have certainly stimulated housing demand there and are partly responsible for the rapid — and likely unsustainable — rates of appreciation in many markets across the state,’’ Stan Humphries, chief economist at Zillow, said in a statement.

Home buyers seeking the federal benefit had to sign contracts by April 30 to qualify for a tax credit of up to $8,000 and have until Sept. 30 to complete their purchases. In California, buyers could qualify for a credit of up to $10,000 under a program that began May 1.

Foreclosures reached a high in June, with more than one of every 1,000 homes taken over by lenders, Zillow said. The number of properties receiving a notice of default, auction, or bank seizure climbed in three-quarters of US metropolitan areas in the first half of 2010, Irvine, Calif.-based RealtyTrac Inc. said on July 29

Associated Press August 10, 2010

Monday, August 16, 2010

MORTGAGE NEWS: 43 loan originators told to stop work

The Massachusetts Division of Banks has issued 43 temporary cease-and-desist orders against licensed mortgage originators in Massachusetts for failing to meet licensing requirements under updated laws.

Mortgage loan originators must complete 20 hours of prelicensing education, pass both state and national tests, and submit fingerprints for a criminal background check, the division said in a news release yesterday.

State officials released a list of mortgage originators who failed to comply with those provisions before the deadline in the law. They “had ample opportunity to meet the revised licensing requirements,’’ said Steven L. Antonakes, the commissioner of banks. “The division made it clear that any mortgage loan originator that failed to meet all requirements for licensure by the stated deadlines would be unable to continue to do business.’’

Boston Globe August 10, 2010

Mortgage loan originators must complete 20 hours of prelicensing education, pass both state and national tests, and submit fingerprints for a criminal background check, the division said in a news release yesterday.

State officials released a list of mortgage originators who failed to comply with those provisions before the deadline in the law. They “had ample opportunity to meet the revised licensing requirements,’’ said Steven L. Antonakes, the commissioner of banks. “The division made it clear that any mortgage loan originator that failed to meet all requirements for licensure by the stated deadlines would be unable to continue to do business.’’

Boston Globe August 10, 2010

Sunday, August 15, 2010

LOCAL NEWS: Rentals harder to find, afford. Surge in foreclosures in region transforms market for apartments

The region’s rental market has tightened in recent months, with apartment vacancies falling and rents rising for the first time since the beginning of the economic crisis. Analysts said the changes, while small, signal a market shift that is making apartments harder to find and afford when many families are struggling with lost jobs, lost homes, and pay cuts.

A year ago, landlords were chasing renters with price cuts and enticements to combat high vacancy rates. Now, tenants are competing for fewer available units, as surging foreclosures force more people into the rental market. Meanwhile, tight credit and an uncertain housing market keep many renters from leaving apartments to become homeowners.

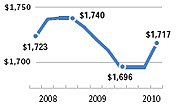

The result: Vacancy rates fell to 6.2 percent in Greater Boston in the second quarter of the year, the lowest level in 18 months, while average asking rents increased for the first time since 2008, rising 1.2 percent to $1,717 a month, according to Reis Inc., which tracks occupancy in buildings with 40 units or more.

“A 6 percent vacancy rate is what you’d expect in a fairly strong economy and that we have that in a weak economy is something quite extraordinary,’’ said Barry Bluestone, dean of the School of Public Policy and Urban Affairs at Northeastern University. “I worry about these things because all the analysis shows that we continue to see less and less affordability, relative to income.’’

The rental squeeze is being felt from triple-deckers in working-class neighborhoods to luxury buildings in downtown Boston, according to brokers and analysts.

Reginald Fuller is among the renters discovering that apartments are harder to find — and afford.

Forced to seek a new place after his pay was cut in half and his rent increased by $150 a month, Fuller has searched for three months to find a new apartment for his family. Now, just weeks from eviction, Fuller worries that he, his wife, Louanna Hall, his 10-year-old nephew, and his 67-year-old father-in-law will end up in a shelter.

“It makes me kind of feel like I let my family down,’’ said Fuller, 53. “I’m about to join the ranks of the homeless, and that’s a place I’ve never been.’’

Foreclosures, on track to break record levels, are a key contributor. Lenders seized 1,300 Massachusetts homes in June, twice as many as a year earlier, according to the Warren Group, a Boston company that tracks local real estate. Completed foreclosures totaled 7,431 in the first half of 2010, up 57 percent from the same period last year.

In Boston, foreclosures have reduced the supply of apartments as banks, unwilling to be landlords, evict tenants and shutter buildings.

Average asking rents in Greater Boston

A year ago, landlords were chasing renters with price cuts and enticements to combat high vacancy rates. Now, tenants are competing for fewer available units, as surging foreclosures force more people into the rental market. Meanwhile, tight credit and an uncertain housing market keep many renters from leaving apartments to become homeowners.

The result: Vacancy rates fell to 6.2 percent in Greater Boston in the second quarter of the year, the lowest level in 18 months, while average asking rents increased for the first time since 2008, rising 1.2 percent to $1,717 a month, according to Reis Inc., which tracks occupancy in buildings with 40 units or more.

“A 6 percent vacancy rate is what you’d expect in a fairly strong economy and that we have that in a weak economy is something quite extraordinary,’’ said Barry Bluestone, dean of the School of Public Policy and Urban Affairs at Northeastern University. “I worry about these things because all the analysis shows that we continue to see less and less affordability, relative to income.’’

The rental squeeze is being felt from triple-deckers in working-class neighborhoods to luxury buildings in downtown Boston, according to brokers and analysts.

Reginald Fuller is among the renters discovering that apartments are harder to find — and afford.

Forced to seek a new place after his pay was cut in half and his rent increased by $150 a month, Fuller has searched for three months to find a new apartment for his family. Now, just weeks from eviction, Fuller worries that he, his wife, Louanna Hall, his 10-year-old nephew, and his 67-year-old father-in-law will end up in a shelter.